Fourth Quarter 2025 Review: Unexpectedly Smooth Sailing

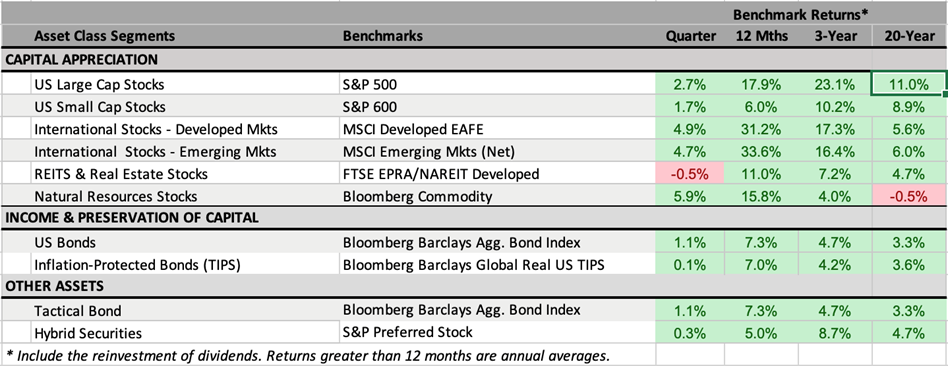

The fourth quarter of 2025 saw markets shrug off sluggish U.S. job growth and a record-long 45-day government shutdown to expand on strongly positive returns for virtually every asset class (Figure 1.1). The Federal Reserve cut interest rates twice in the quarter (and 3 times in the final 4 months of the year), reducing the Fed Funds rate by a cumulative 0.75%. Looser monetary policy, amid strong profit growth and subdued inflation, buoyed stock and bond returns.

Figure 1.1

U.S Large Cap Stocks

For the third consecutive year (and the 6th of the last 7 years), the S&P 500 delivered a positive double-digit return. However, it was a rocky path: the index was down approximately 15% through April 8th, only to rally almost 39% from April 9 onward, finishing the year up nearly 18%. Once again, a small cohort of large technology companies drove performance, and this handful of companies now accounts for a strikingly large proportion of the index (at year-end, the top 10 constituents in the S&P 500 comprised almost 41% of its value).

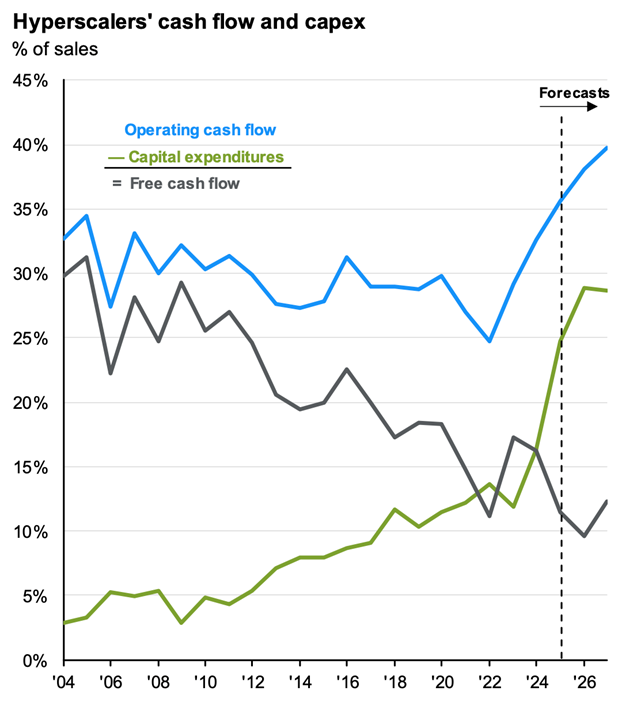

As discussed in our Q3 Commentary, the AI “Hyperscalers” remain among the most profitable companies on the planet. However, they are now diverting a much higher proportion of their operating cash flow into capital expenditures (Figure 1.2), fundamentally changing the capital intensity of their businesses, and (arguably) the risk/reward proposition for investors. Free cash flow (the cash a business has left over after it runs its day‑to‑day operations and pays for big investments like equipment and buildings) as a percentage of sales for this cohort has declined by nearly two-thirds in the last two decades, reducing the amount available for distribution to shareholders via dividends and share repurchases.

Figure 1.2 - Source: JP Morgan Guide to the Markets, 12/31/25

Figure 1.2 - Source: JP Morgan Guide to the Markets, 12/31/25

U.S Small Cap Stocks

Returns for smaller-company stocks in 2025 varied somewhat by quality, as seen in the disparate returns of the S&P 600 Index (+6%) and the Russell 2000 Index (+12.8%). Both indexes track a universe of small-company stocks, but the former employs strict qualitative criteria to filter out unprofitable companies, while the latter does not (notably, about 40% of the companies in the Russell 2000 Index are unprofitable).

Three interest rate cuts in the final third of the year had a more pronounced positive impact on investor appraisals of heavily indebted, marginally profitable companies than on those of higher-quality peers in that universe. While we continue to emphasize the S&P 600 as the most appropriate small-cap benchmark in client portfolios, our modest exposure to micro-cap stocks (also highly sensitive to interest rates) helped to bring overall performance for this asset class in line with the Russell 2000, regardless.

International Stocks

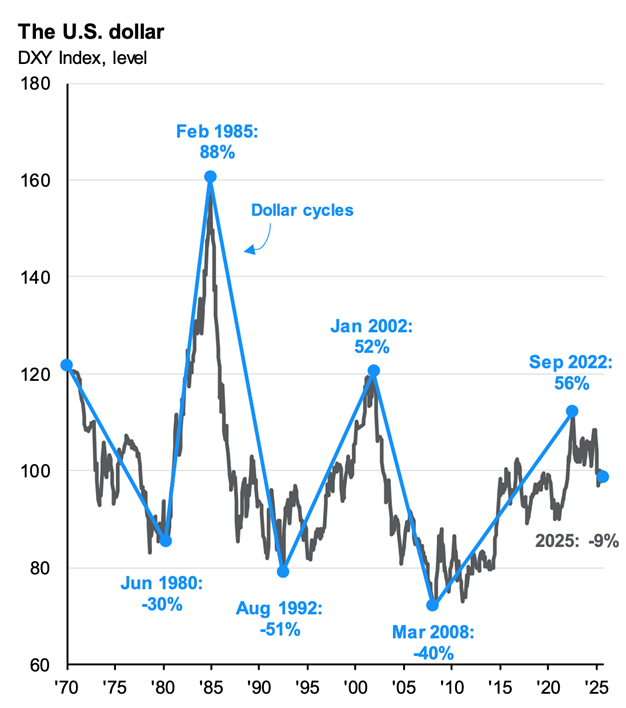

Non-U.S. stocks outperformed the S&P 500 for the first time since 2022, and by the widest margin in at least 15 years. Some—but not all—of that outperformance can be attributed to the declining value of the U.S. Dollar, which weakened by about 9% in 2025 vs. a basket of international currencies, and finished the year about 13% below its recent peak. Cycles of dollar strength and weakness tend to be of multi-year duration, potentially creating a continuing tailwind for U.S. holders of non-U.S. stocks (Figure 1.3).

Figure 1.3 - Source: JP Morgan Guide to the Markets, 12/31/25

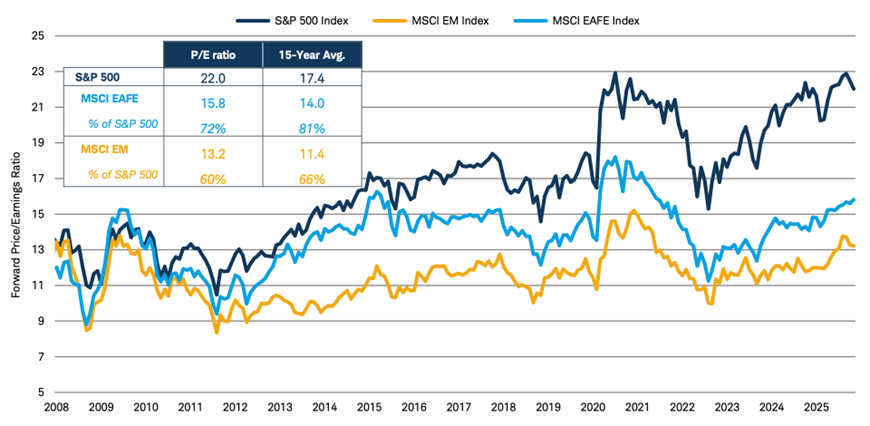

Even without the currency tailwind, international stocks outperformed the S&P 500, with the MSCI All-Cap ex-U.S. Index rising 25.1% in local-currency terms (+33.1% in $USD). Both international developed and emerging market stock valuations remain well below those of the S&P 500 index (Figure 1.4), offering a compelling alternative for investors seeking broader diversification from an increasingly top-heavy U.S. equity market.

Figure 1.4 - Source: Charles Schwab Chartbook, 12/31/25

Commodities & Natural Resources

Commodities were the best-performing asset class in our “capital appreciation” bucket in Q4, and delivered solid returns for full year as well, driven by exceptional gains in precious metals (ex: gold and silver), and industrial metals (ex: copper, aluminum). Foreign central banks, in reaction to geopolitical uncertainty, have been diversifying their U.S. dollar reserves, partly by buying gold and silver (another factor driving down the value of the U.S. dollar). Meanwhile, surging construction of data center infrastructure drove up demand for industrial metals, even as production outages and trade disputes constrained supply.

After gold rallied approximately 60% and silver more than doubled in price in 2025, some clients have wondered why we do not have a more meaningful direct allocation to precious metals. The reason is that while gold has occasionally been an effective diversifier, it has also experienced long periods of value destruction. For example, during the 20 years between 1980 and 2000, the price of gold declined almost 80% in real (inflation-adjusted) terms! Moreover, beyond the fact that gold does not generate any yield, it has also historically been more volatile than U.S. stocks. Thus, a small allocation to a broadly diversified basket of commodities and natural resources seems a more prudent way to access the favorable characteristics of this asset class, without taking on too much risk.

Bonds

Bonds enjoyed an ideal “goldilocks” environment in 2025. The Fed lowered short-term borrowing rates by a cumulative 0.75% even as corporate profits grew, credit spreads narrowed, and inflation moderated. A steepening yield curve drove a solid 7% return for intermediate-term investment-grade bonds (as represented by the Barclays Aggregate Bond Index). Foreign bonds and inflation-protected securities (TIPS) performed equally well. Even money market funds and short-term T-bills delivered returns exceeding core inflation. In fact, 2025 was the best year for bonds (in both nominal and inflation-adjusted terms) since 2020.

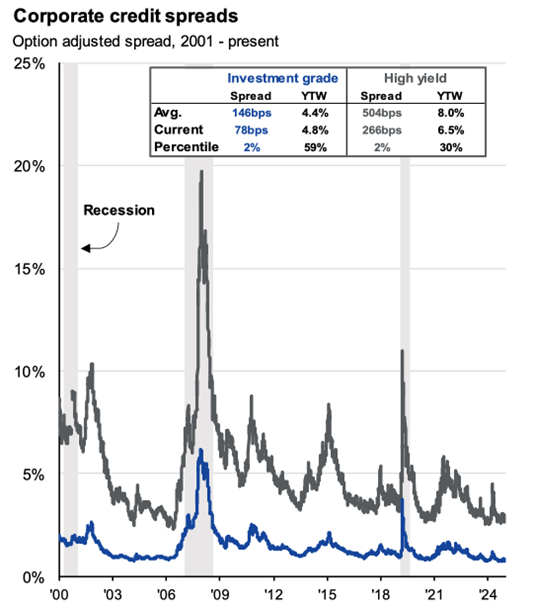

Looking ahead to 2026, some of these tailwinds are likely to dissipate (or at least not recur to the same magnitude). While additional rate cuts are possible, there is no clear consensus among current Fed governors on the need for additional cuts. On the one hand, employment growth is slowing—2025 was the worst year for net job growth (outside of a recession) since 2003. On the other hand, inflation is still running close to 3% and above the Fed’s target of 2%, leaving little room to maneuver. Finally, with credit spreads (the extra yield investors demand to lend to a riskier borrower instead of a safer one) already historically low (Figure 1.5), it is unlikely that they compress further (spreads tend to widen during periods of market volatility or financial dislocation).

Figure 1.5 - Source: JP Morgan Guide to the Markets, 12/31/25

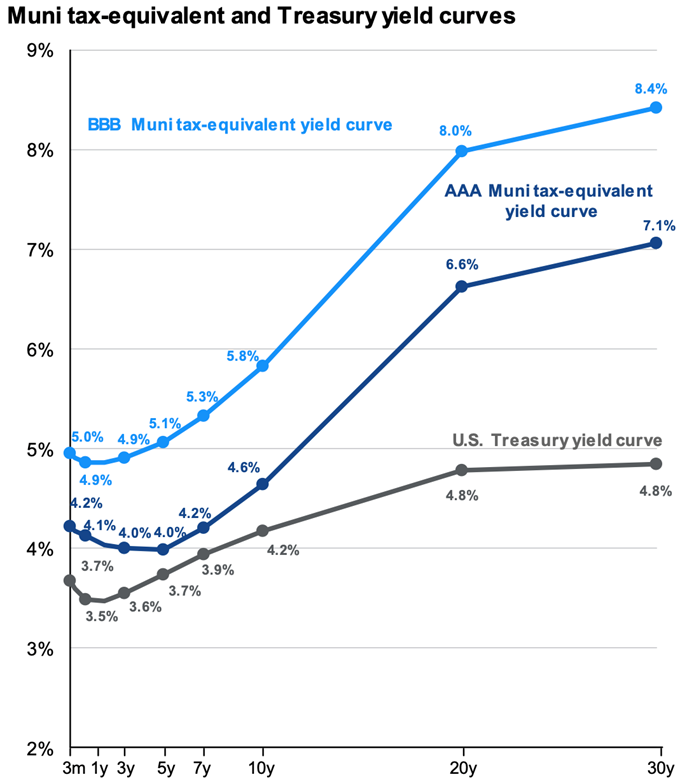

One pocket of relative value in the bond market remains municipal bonds. Even as federal debt has ballooned as a % of GDP over the last 15 years, state and local debt has declined as a % of GDP. Moreover, in the wake of the Great Financial Crisis, many state governments boosted their “Rainy Day Fund” reserves, increasing financial flexibility. Tax-equivalent yields on Muni bonds (for taxpayers in the top bracket) continue to be very attractive compared to U.S. Treasury debt, especially for longer maturities (Figure 1.6).

Figure 1.6 - Source: JP Morgan Guide to the Markets, 12/31/25

Figure 1.6 - Source: JP Morgan Guide to the Markets, 12/31/25

Farewell to the G.O.A.T.

2025 marked another bittersweet milestone: Warren Buffett (age 95) officially stepped down as CEO of Berkshire Hathaway after 60 years at the helm and an unparalleled track record of investment success. Mr. Buffett has long been an inspiration to all of us at Bristlecone, not just for his investing acumen but also for his humility, generosity, wit, and keen sense of ethics.

While we hold little hope of matching his investing success, we strive daily to emulate his strength of character. As Buffett famously noted, “It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.”

2026 Outlook

Heading into the new year, there are reasons for continued optimism about the prospects of diversified stock-and-bond portfolios. Valuations for US Large Cap stocks, while higher than average, have remained steady and are supported by underlying profit growth. Outside the largest U.S. stocks, valuations are more moderate and in line with historical averages, even as monetary policy remains relatively accommodative, and inflation is holding below 3%. Consumer sentiment (typically a contrary indicator for future stock performance) is very subdued.

Finally, the passage of the One Big Beautiful Bill Act (OBBA) in mid-2025 made several permanent tax cuts scheduled to expire in 2026 and introduced several new tax breaks, effective retroactively from January 1, 2025. For this reason, analysts expect the average taxpayer to benefit from a higher tax refund in 2026, providing additional fiscal stimulus in the first half of the year.

Our focus continues to be on maintaining the sort of low-cost, balanced, diversified portfolios that we think give our clients the best chance at weathering stock market volatility and achieving their long-term financial objectives.

As always, we appreciate your confidence in Bristlecone and welcome any comments or questions you may have. We wish you and your families a prosperous and healthy 2026.

One of Bristlecone Value Partners’ principles is to communicate frequently, openly and honestly. We believe that our clients benefit from understanding our investment philosophy and the process behind it. Our views and opinions regarding investment prospects are "forward-looking statements," which may or may not be accurate over the long term. While we believe we have a reasonable basis for our appraisals and confidence in our opinions, actual results may differ materially from those we anticipate. Information provided in this blog should not be considered as a recommendation to purchase or sell any particular security. You can identify forward-looking statements by words like "believe," "expect," "anticipate," or similar expressions when discussing particular portfolio holdings. We cannot assure future results and achievements. You should not place undue reliance on forward-looking statements, which speak only as of the date of the blog entry. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Our comments are intended to reflect trading activity in a mature, unrestricted portfolio and might not be representative of actual activity in all portfolios. Portfolio holdings are subject to change without notice. Current and future performance may be lower or higher than the performance quoted in this blog. References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest directly in an index, and returns do not account for the deduction of advisory fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio, and there can be no assurance that a portfolio will match or outperform any particular index or benchmark. Past Performance is not indicative of future results. All investment strategies carry the potential for profit or loss. Changes in investment strategies, contributions, or withdrawals can materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio. This content is developed from sources believed to provide accurate information, and it may not be used to avoid any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.